What Entrepreneurs Need to Know About Tax Planning

Beginning your entrepreneurial career is thrilling, isn't it? However, as soon as you begin, there is one word that silently stares at you from every corner: taxes.

Yes, the less glamorous but equally important aspect of running a business. If you think taxes are just a yearly hassle, you're losing out on a significant piece of the puzzle.

Proper tax planning is not about paying less dishonestly; rather, it is about strategically placing your organization to save money, remain compliant, and even grow quicker.

In this guide, we'll cover all you need to know about tax preparation, from the fundamentals to practical methods, recommendations, and real-world examples. Scroll through, step by step, and you'll have a clear plan for dealing with taxes like an expert.

Why Entrepreneurs Cannot Ignore Tax Planning

Taxes are sometimes viewed as a "problem to be solved later." However, if you wait until the end of the fiscal year, you're likely to find yourself scrambling, missing deductions, and paying more than necessary.

Think of tax planning as a road map for your company's finances. When done correctly, it's like having a personal GPS directing you down the winding highways of financial commitments. Here's why it matters:

- Cash Flow Control: Effective tax planning ensures that your cash flow remains predictable. You'll know how much to set aside for taxes, avoiding unpleasant surprises at year-end.

- Reduced Tax Liability: Strategic planning can lawfully reduce your taxable income through deductions, credits, and exclusions.

- Avoid Penalties: The tax officials are not joking. Late payments or mistakes can be quite costly. A proper plan will keep you compliant.

- Business Growth: Money saved through savvy tax techniques can be reinvested in the company for marketing, hiring, or product development.

So, if you want to stay ahead, tax preparation is not an option; it is a critical component of your strategy.

Understand the Types of Taxes that Every Entrepreneur Faces

Before we go into tactics, let's clarify the kind of taxes you're dealing with. Many entrepreneurs become lost because they don't know what's relevant to them. Here is a simple breakdown:

- Income Tax: Any profits you make as a sole proprietorship, partnership, or company are taxable. Making a plan ahead of time will help you pay less.

- Corporate Tax: Registered firms' profits are taxed differently than personal income. Understanding company structures might help you save money.

- Services Tax (GST) / VAT: If your company sells goods or services, indirect taxes apply. Keeping track of collections and payments is critical.

- Payroll taxes: It refers to deductions, contributions, and compliance. Missing payroll taxes can be expensive.

- Other Local Taxes: Municipal, property, or license-based taxes may exist in your location.

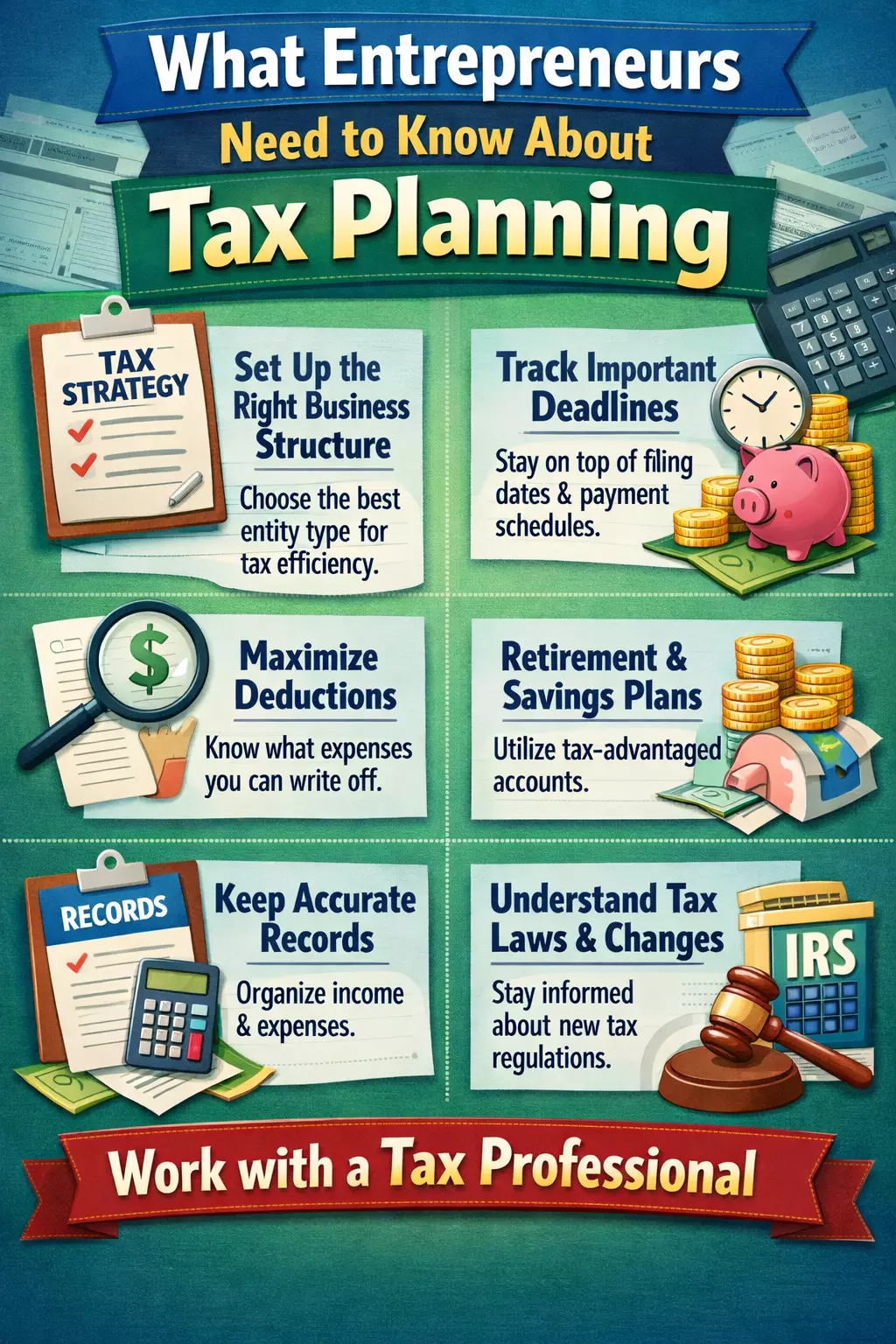

The Fundamentals of Tax Planning: Timing and Organization

This is where the majority of entrepreneurs stumble. They believe that "I'll sort it out later." A big mistake. Tax planning entails managing your finances now to save money later. Here's how you approach it:

- Maintain accurate records: Keep track of all expenses, invoices, and receipts. It may appear monotonous, yet these figures constitute the foundation of deductions.

- Maintain separate business and personal accounts: Mixing finances is a tax nightmare. Keep your accounts absolutely distinct.

- Plan quarterly: Do not wait until the end of the year. Estimate your taxes quarterly. This prevents surprises and penalties.

- Track Deductible Expenses: Understand what really matters, from office rent to software subscriptions. Every modest savings adds up.

- Consider this the foundation-laying stage: Without adequate records and structure, the rest of the approach will be meaningless.

Deductions and Credits Are Your Secret Weapons

Here's the thing: while paying taxes is unavoidable, paying more than necessary is not. Deductions and credits are legal techniques to decrease liability.

- Home Office Deduction: If you run your business from home, you may be able to deduct some of your rent, utilities, and internet expenses.

- Business Expenses: Equipment, software, travel, and even meals (with restrictions) can reduce taxable revenue.

- Retirement Contributions: Contributions to retirement programs for yourself or employees are tax deductible.

- Education and Training: Business-related courses, certifications, or seminars may be eligible for deductions.

- Energy Credits: Some regions offer credits for using renewable energy or doing environmentally friendly modifications.

The Impact of Choosing the Right Business Structure

Did you realize that the type of business you operate has a direct impact on the amount of tax you pay? That is why many savvy entrepreneurs reconsider structure early on. Your decision affects deductions, liabilities, and future growth potential.

Planning your structure with taxes in mind provides a long-term benefit. Here is a compiled pointer so you understand this correctly.

- Sole Proprietorship: Easiest to establish, but profits are taxed at personal rates.

- Partnership: Shared obligations and taxes; earnings are distributed but taxed individually.

- Limited Liability Company (LLC)/Private Limited: Provides protection and potential tax benefits.

- Corporation: Can be taxed at lower corporate rates, but compliance costs more.

Timing is Everything: Strategic Income and Expense Planning

Deciding when to collect income or spend money is an important part of tax planning. Simple timing tweaks can save thousands.

These little, intentional steps are what distinguishes a tax-savvy entrepreneur from one that is continually struggling. Divide your income like this:

- Defer Income: If you expect reduced revenue next year, delaying income to the following year can lessen your current year's taxes.

- Accelerate Expenses: Paying some expenses before the end of the year might improve deductions for the current tax year.

- Balance Assets and Liabilities: Buy assets strategically; some may provide depreciation benefits.

Stay Current: How to Keep Up With Changes in Tax Laws

Tax regulations change every year. What worked last year could not work now. Many entrepreneurs miss out on chances because they adopt obsolete tactics. Consistency and vigilance here minimize costly mistakes and ensure that your plan is future-proof.

- Follow any updates from your tax authority

- Consult an accountant or tax professional who is up to date on the latest modifications.

- Adjust deductions, credits, and planning to reflect updated rules:

Use Technology for Better Tax Planning

Do not underestimate the power of tools. Technology can automate, organize, and even forecast your tax liabilities.

- Accounting software: like QuickBooks, Zoho Books, and Xero, can easily track income, costs, and deductions.

- Expense trackers: Apps like Expensify can help you keep track of receipts and categorize your costs.

- Tax filing tools: TurboTax or ClearTax can help you compute taxes accurately and suggest deductions.

Common Mistakes to Avoid in the Future

Even the most successful entrepreneurs fall short when it comes to tax planning. Avoid the following pitfalls:

- Mixing personal and business finances – chaos for deductions and audits.

- Ignoring small deductions – every dollar counts.

- Procrastinating – waiting until year-end leads to missed opportunities and penalties.

- Not consulting professionals – DIY is fine, but a professional can spot savings you may never see.

Read: Year End Tax Planning Tips for Business Owners and Sales

Step-by-Step Guide to Implementing Tax Planning

Tax planning does not have to be a headache. With the appropriate strategy, you can control your money rather than react to it. Here's the roadmap we provide to every entrepreneur looking to stay ahead:

- Get Organized: Keep your accounts, receipts, and invoices organized. An organized system now saves hours of confusion later.

- Analyze Your Tax Situation: Determine which taxes apply to your firm and estimate potential liabilities. Awareness is only half the battle.

- Maximize Deductions and Credits: Determine each lawful deduction and credit available. From home office bills to business trips, ensure nothing falls between the gaps.

- Examine Your Business Structure: Your current structure may not be the most tax efficient. Consider whether switching could save money.

- Plan Your Income and Expenses: Timing is important. Smartly schedule payments and income to decrease taxable responsibilities to the greatest extent practicable.

- Use the Right Tools: Accounting tools, cost trackers, and tax calculators can help you plan more effectively and minimize mistakes.

- Annual Review: Tax laws change as your business evolves. To keep ahead, review your plan once a year.

- Consult Professionals: When in doubt, don't hesitate to consult with a CPA or tax specialist; they're an investment in your peace of mind.

Final Thoughts!

We hope this guide has cleared up any confusion about taxes for your business. To succeed as an entrepreneur, you must be watchful, implement the appropriate plans, and adapt as restrictions change.

Remember, tax preparation is not a one-time task; it is an essential component of running a successful business.

Every phase, Errizo, from deductions to timing to business structure, works together to save you money, protect you from fines, and provide funds for future growth.

Take control of your taxes today and see how a well-planned strategy can make your entrepreneurial path easier, more profitable, and less stressful.