Term Life Insurance Rates by Age Chart Guide

This is a chart that breaks down term life insurance rates by age; premiums increase monthly or yearly because insurers are pricing the policy according to mortality risk, health profile, policy length and amount of coverage.

The average best term life insurance rates by age chart will be a guide for most U.S. consumers comparing side-by-side quotes, but not the final price, since each insurer has its own underwriting criteria.

Insurance rates by age: term life insurance rate comparison chart helps consumers calculate the average insurance cost by age before requesting quote. The chart is usually something showing sample premiums for a level death benefit such as $250,000 or $500,000 across ages(gender may change it), tobacco status, health class and length of the policy.

Age remains one of the most powerful negative pricing signals for Life and Health Insurance in U.S. every year alone will add to expected mortality risk.

For example, a healthy 30-year-old nonsmoker might qualify for low level term life insurance premiums while the same death benefit might be several times more expensive for an applicant at age 55 with tobacco use or chronic health conditions.

What is an Actual Term Life Insurance Rates by Age Chart?

A term life insurance rates by age chart analyzes sample premium shift across age bands. It will not secure an approval or a locked-in price and is not a substitute for your own quotation.

The best part of the chart is that it indicates how pricing works: most premiums increase gradually throughout young adulthood, but fast as you age into your 40s, then really explode in expense in your 50s, 60s and also 70s.

Term life insurance is actually a subset of the bigger life insurance category. Its relationship to family life insurance plans the simplified version term coverage is very often aligned with securing temporary liabilities (example: mortgage, kids schooling expenses, income replacement for the home, unresolved debts).

Whole life and other types of permanent life insurance, on the other hand, serve a different purpose since they are intended for coverage during your entire lifetime (and can include cash value).

An age-based life insurance rates by age chart should clearly specify the modeled policy type, coverage amount, duration of term, risk class (i.e. Rate comparisons can be worthless without those assumptions, because a $250,000 10-year term policy is not even the same kind of product as a $1 million 30-year term policy.

Life Insurance Rates Increasing as we age

Mortality, interest assumptions and insurer costs are used to create life insurance prices. Mortality is the anticipated chance the insurer will no need to pay a death benefit throughout of the $100,000 coverage time period.

Assumptions around interest rates ultimate express how insurers invest the premiums they receive. Lines of Expense: covers administration, underwriting, commissions, compliance and policy servicing.

Age directly affects mortality assumptions. For instance, a healthy 25-year-old typically has a lower risk of dying over a 20-year term than does a healthy 55-year-old. The insurer builds the premium difference into the coverage, even though both applicants request the same amount of coverage.

The pricing gulf can also be widened by simple health and lifestyle factors. Use of tobacco, high blood pressure, diabetes, obesity, dangerous jobs and hobbies as well as information included in family medical history charts and driving records may move an applicant from a preferred class into a standard or rated class. That change can raise premiums above age alone.

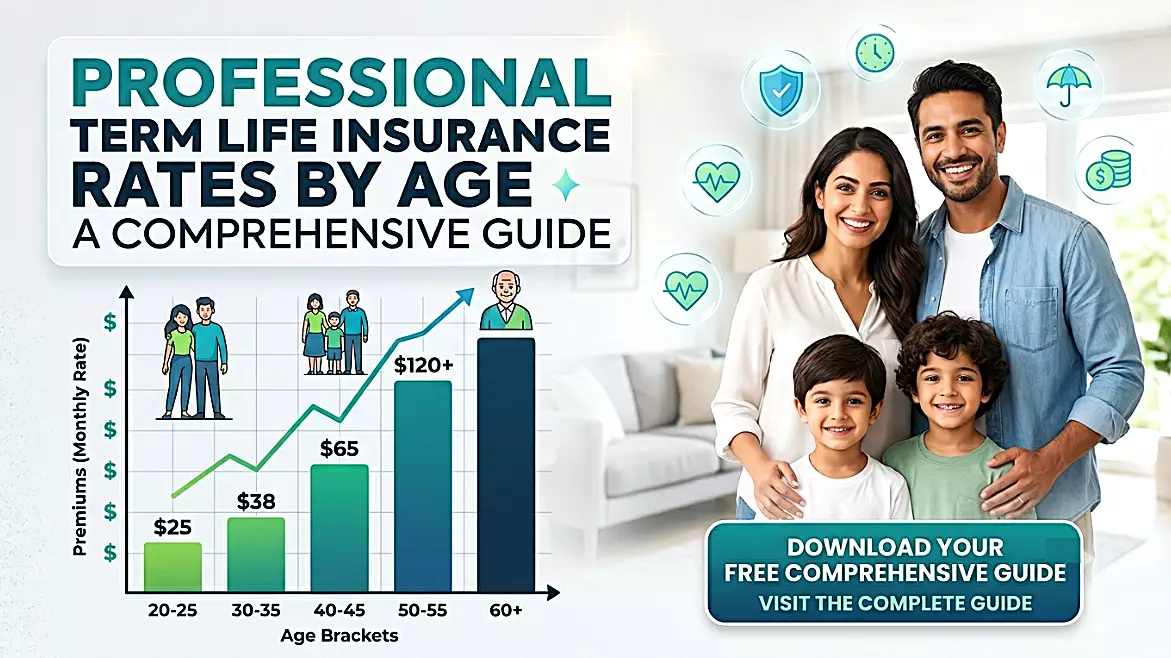

Typical Term Life Insurance Rates by Age

Most age based term life insurance rates by age chart are based off a sample policy (such as a $500,000, 20 year term for healthy non-smokers) although you can exclude any value but the age bracket.

New market examples suggest a relatively low annual premium for applicants in their 20s and 30s, but those in their 50s and most certainly early-60s may face much steeper price jumps from preferred non-smokers.

Here are some general ranges of our sample preferred-plus annual rates for $500,000 20-year term policies:

- Age 20: approximate mid-$100s to low-$200s per year for healthy nonsmokers.

- Age 30: still often low-$200s-per-year for healthy applicants.

- Age 40: Generally a few $high-$200s and $low-$300s per year

- At $600 to $800+ each year: Age 50.

- 60 Years Old: Could skyrocket to $1,600 to over $2,300 per year.

Industry Age 70 is within a few thousand dollars per year, subject to grasp and insurer appetite.

Ultimately the best term life insurance rates by age are read as a time signal. Earlier coverage will secure a fixed premium for the chosen policy duration. Delaying can come with higher costs for the same death benefit and a different diagnosis may result in lower qualifications or higher premiums.

Level Term Life Insurance and Why it is important

Level term life The premium and the death benefit for level term life insurance remains unchanged for the duration of an elected period (10, 15, 20, or even as long as 30 years). This arrangement is beneficial to household budgeting because there is an upfront monthly cost for the consumer.

Family obligations decline over time, and so a 20-year level term policy is often matched to family dilemmas. Parents will use it until children are self-supporting. It can be used by homeowners to fill this gap till the remaining mortgage period. Some business owners might also use it to secure a loan or buy-sell agreement.

The key tradeoff is duration. Shorter duration is less expensive because the insurer has risk for fewer years. The further you protect into older ages, the higher the cost, which is why a longer term is more expensive. Instead of simply picking the cheapest quote available consumers need to check term length vs. actual financial commitment.

How whole life insurance quote comparison: Mortality rates by age

A different product type is measured by a whole life insurance rates by age chart. Whole life is permanent life insurance coverage specifically meant to continue as long as the insured lives, assuming premiums are paid. It typically has both guaranteed components and a cash value aspect.

This is why whole life insurance costs are so much more expensive than term life, as this policy remains in force for your entire lifetime versus just a limited term. Someone who is a healthy 30-year-old nonsmoker might pay multiples more, like four times more, for a $500,000 whole life policy than they would for a $500,000 20-term policy.

Equally important, long-term needs should be compared with the average cost of whole life insurance. Whole life might work for estate planning, care of an heir permanently unable to live independently, business succession or final-expense plans you want to continue all your life.

This is not typically the least-expensive method for generating a large income-replacement benefit while you are still in the workforce.

How Much Does Permanent Life Insurance Cost/Permanent Cash Value

Part of the premium for permanent life insurance cost is lifetime insurance protection, plus a cash value feature included in many policies. Common permanent policy categories include whole life, universal life, indexed universal life and variable life but operate differently.

Whole life generally has fixed premiums and more consistent guarantees. While universal life allows for flexible funding of the premiums, the policy must still be funded sufficiently to remain active. Variable Life may also subject cash value to the performance of investments - giving cash value growth potential but subjecting them to market risk.

It is a mistake to make an apples to apple comparison of permanent life insurance cost vs. Term insurance, without knowing the purpose Term life is basically insurance for a set period of time. Permanent life is insurance plus a policy framework that, at least indirectly, “savings type” or “investment linked” elements.

Guaranteed Issue Life Insurance

It is typically whole life insurance (a coverage type that lasts your lifetime if you main benefit of guaranteed issue life insurance is the fact it tends not to come with a medical exam or health questions. It is beneficial for older adults or applicants if there are serious health issues but cannot pass a traditional underwriting

The cost that you incur and the magnitude of benefits that you get in return. These facts lead to lower death benefits, higher premiums per dollar of coverage, and a graded death benefit period since most guaranteed-issue policies are offered with a 2–3 year graded benefit period. Natural cause of death does not result the complete death benefit during the graded period.

The only time you should treat your guaranteed issue life insurance as anything more than a last-resort coverage option. For healthier applicants comparing fully placed term, simplified-issue-term and traditional whole life will provide the essential information needed to avoid guaranteed acceptance coverage.

Read: How Term Insurance Demand Is Evolving In The Digital Era

How to Properly Read Life Insurance Rates by Age

Note that a life insurance rates by age chart helps when the assumptions made reflect with reality of the buyer. In other words, a quote for a 25-year-old preferred non-smoker is not going to help out an applicant who is 48 years old and has controlled diabetes unless health-class differences are also charted.

These inputs should be reviewed by consumers when comparing quotes:

- Age at application.

- Gender used for underwriting.

- Tobacco or nicotine status.

- Current and past medical conditions.

- However you'll also see here it says type of policy: domain name, complete survival, global life or guaranteed problem etc.

- Design covering short-term and term length of life.

- Death benefit amount.

- Functions of the state availability and insurer underwriting rules.

- For example, waiver of premium or child term rider, or accelerated death benefit.

- Cheapest policy is not the best policy. It should also be a strong quote: proper term length, good conversion options, clear renewal language, and an insurer with solid financial health.

Real-World Application: Three Buyer Examples

Example: 32 year old married parent with two young children selects a $750,000 20-year level term life insurance. The purpose being income replacement, support for childcare, protection for your mortgage and funding of education. This scenario runs across most term insurance since the need is voluminous but urgent.

Example: A 47-year-old business owner by purchasing some combination of term and permanent coverage. Term life is available for 15 to 20 years that can cover a business loan or income obligation. Whole life or even another sort of permanent policy might help fund a business succession, provide estate liquidity, or be used to care for a planning-dependent close friend in the future.

A retiree age 68 with no mortgage, and adult children to care for after he is gone, might need only final-expense coverage.

For medically eligible retirees a traditional whole life policy may be much more efficient than guaranteed issue life insurance. Guaranteed issue with limited consumer protection when various chronic health conditions you have prevent approval from being granted, is not possible unless a graded period is applied.

Ways to Reduce Cost of Life Insurance by Age

Applying for life insurance before health issues arise is the single most impactful way to reduce how expensive it will be, especially when achieving a low quote by age. Time may not reverse the age but can improve pricing. So, a healthy applicant buying at 35 may receive a lower level premium than that experienced by the same yet older applicant who buys at age 45.

Policy design also affects cost. By choosing the right term length, you can avoid paying for years that may not be needed. So match your coverage with what you are actually responsible for, this prevents you from going over or under on insurance policy.

To apply for health insurance consumers must prepare their medical information ahead of time to get accurate quotes. Factors like current prescriptions, what physicians a person has recently seen and lab results are aiding insurers in better assessing risks as well as the applicant's tobacco history, height/weight, also income, debts, existing coverage.

People Also Ask: FAQs

Step-by-Step: Best Age to Buy Term Life Insurance

Term insurance is at its best stage when a person has just begun their life with financial dependents or huge debts. Purchasing earlier usually results in lower premiums, but coverage should align with an actual financial need rather than age.

Cost of nonmed term life insurance by age

The cost of term life insurance by age: like other types of life coverage, depends on the applicant's health status, tobacco use status at the time the policy is written; gender; amount of insurance desired, and length/type of term. The lowest rates are usually reserved for healthy nonsmokers in their 20s and 30s, and premiums tend to increase more quickly after the age of 40.

Should you buy whole life insurance instead of term?

However, whole life insurance is not automatically superior to term life insurance. Whole life is also meant for permanent coverage and cash build-up, while term life is intended to be a lower-cost policy for a restricted amount of time. Which of these two is a better option depends on the financial goal.

Why is life insurance for smokers more costly?

When assessing insurability, tobacco use increases mortality risk and smokers have more expensive life insurance. Insurers build that increased risk into premiums, and smoker rates can be several times higher than nonsmoker rates for the same policy.

Is family life insurance plans worth for money?

Family life insurances plans can be worth it if they cover certain household risks (i.e. which will be lost by the reliance of header and has to bear additional costs like childcare, debts, final expenses). The optimum family plan generally offers proper coverage amounts, practical term lengths, and cost-effective premiums.