Term Insurance vs Endowment Plan: Which One Should You Actually Buy?

Every week, someone walks into our office having paid premiums on an endowment plan for 5–10 years, only to realise the cover is nowhere near what their family actually needs.

The policy was sold as "insurance plus savings" — which sounds sensible — but when you do the actual maths, neither the insurance nor the savings part is doing its job well.

This confusion between term insurance and endowment plans has cost Indian families crores in lost wealth and inadequate protection. So here is a clear, honest breakdown of what each product actually does, where each one makes sense, and the specific situations where one is the wrong choice entirely.

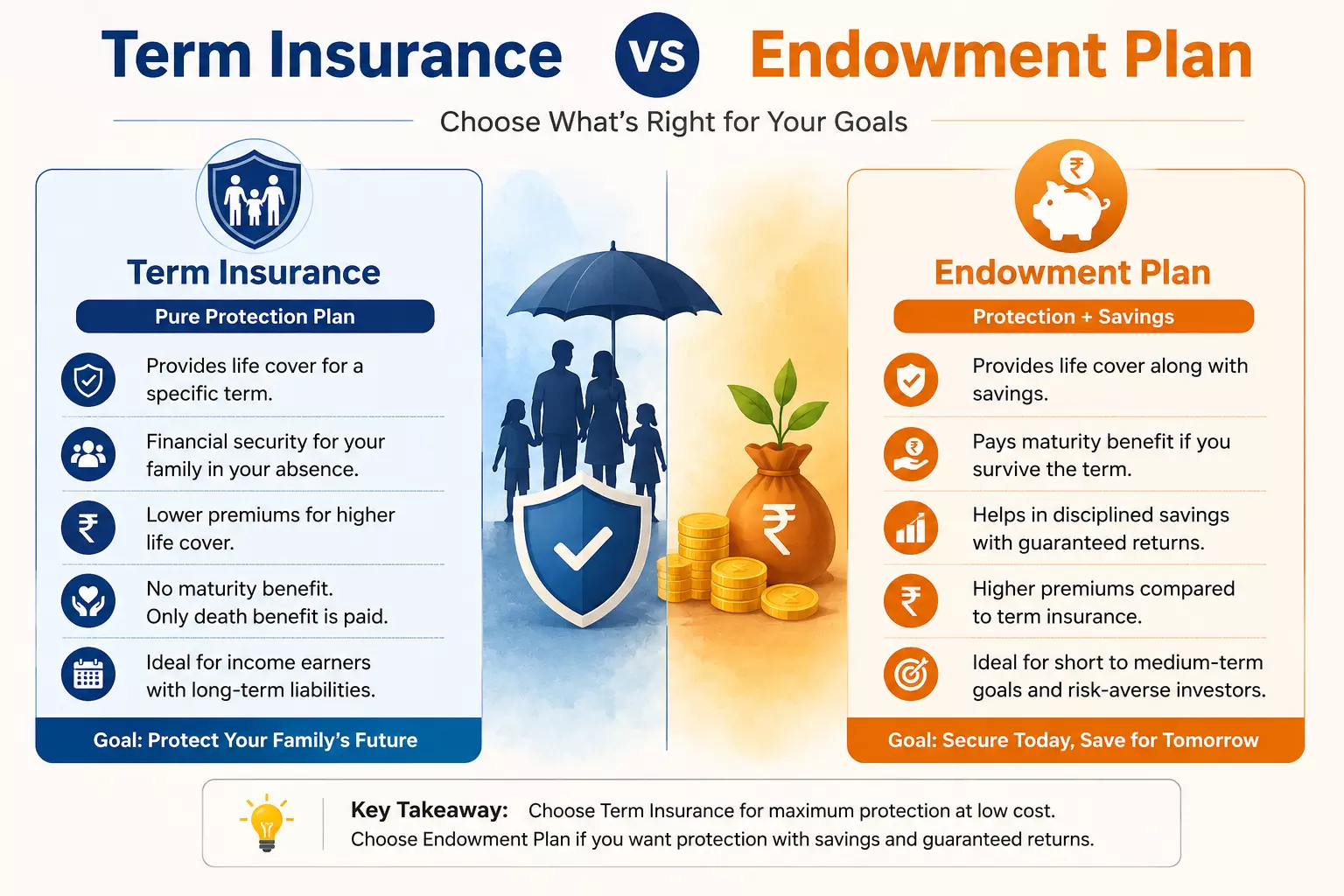

What Is Term Insurance?

Term insurance is pure life cover. You pay a premium every year, and if you die during the policy term, your nominee receives the sum assured. If you survive the term, you receive nothing back — no maturity amount, no bonus, no refund.

That last part is what makes people hesitant. "I get nothing if I survive?" — yes, and that is exactly what keeps the premium low. You are paying for protection, not savings.

Think of it the same way you think about car insurance. You pay the premium every year. If you don't have an accident, you don't get your money back. Nobody calls that a bad deal because the whole point was protection against a risk.

Term insurance works on the same principle — it protects your family's financial life against the risk of your early death, at the lowest possible cost.

What Does Term Insurance Cover?

A standard term plan pays the full sum assured to your nominee in the event of your death during the policy period. Most plans today also allow add-on riders — critical illness cover, accidental death benefit, waiver of premium on disability — which can be added at a marginal additional cost to make the base plan more comprehensive.

The sum assured is typically recommended at 15–20 times your annual income, factoring in outstanding loans, future income replacement, and inflation.

What Is an Endowment Plan?

An endowment plan bundles life insurance and savings into a single product. You pay a higher premium, and the plan does two things: it provides a death benefit if you pass away during the term, and it pays a maturity amount — your premiums plus accumulated bonuses — if you survive the full term.

This bundling is the core of the endowment plan's appeal, and also the source of most of its problems. When you combine two very different financial needs — protection and wealth creation — into one product, you end up with a product that does neither particularly well.

How Is the Endowment Premium Structured?

A portion of your premium goes toward the mortality charge (actual insurance cost), a portion goes into a savings pool that the insurer manages and invests, and a significant portion covers the insurer's operating costs, agent commissions (often 25–40% of the first year's premium), and fund management expenses.

What remains generates the bonus that gets added to your policy over time.

This layered cost structure is why endowment plans deliver returns of only 4–6% CAGR, even when the insurer is earning 8–10% on its investment portfolio. The gap between what the insurer earns and what you ultimately receive is absorbed by these costs.

The Premium Difference — This Is Where It Becomes Obvious

This is the number that settles the debate for most people once they see it.

A 30-year-old non-smoker wanting ₹1 crore life cover for 25 years:

Term insurance: Annual premium of approximately ₹10,000–12,000. Total paid over 25 years: roughly ₹2.5–3 lakh.

Endowment plan for ₹1 crore sum assured: Annual premium of approximately ₹4–4.5 lakh. Total paid over 25 years: roughly ₹1 crore–1.12 crore.

That gap — roughly ₹4.38 lakh per year — is the amount that goes into the endowment plan's savings component above what you'd have paid for the same cover via term insurance. If you invested that ₹4.38 lakh annually in a mutual fund SIP earning 10% annually, your corpus after 25 years would be approximately ₹4.9 crore.

The endowment plan's maturity value over the same period, assuming 5% CAGR: approximately ₹1.7 crore.

The difference between these two outcomes — ₹4.9 crore versus ₹1.7 crore — is not a rounding error. It is roughly ₹3.2 crore in wealth that the bundling of insurance and investment quietly costs you.

This is the "buy term, invest the difference" principle that nearly every independent financial advisor in India recommends — and it is mathematically difficult to argue against.

What Changed After September 2025?

One important update that affects both products: from September 22, 2025, individual life insurance premiums — including both term insurance and endowment plans — are no longer subject to 18% GST. This makes both products effectively cheaper than they were a year ago.

For term insurance buyers, this is a straightforward premium reduction. For endowment plan buyers, it reduces the total outflow slightly, but it does not change the underlying return structure or the cost gap with term plans.

Additionally, IRDAI's new Special Surrender Value rule now allows endowment policyholders to exit and receive a refund after paying just one year of premium. Previously, surrendering in the early years meant losing most of what you had paid.

This change gives endowment policyholders more flexibility if they realise mid-way that the product isn't right for them — a meaningful improvement in policyholder protection.

Term Insurance vs Endowment Plan: A Direct Breakdown

Purpose:

Term insurance — pure life protection; nothing else.

Endowment plan — life protection bundled with a savings/investment component.

Premium for ₹1 crore cover (30-year-old, 25-year term):

Term insurance — approximately ₹10,000–12,000 per year.

Endowment plan — approximately ₹4–4.5 lakh per year.

Maturity benefit:

Term insurance — nil (unless Return of Premium variant, which costs significantly more).

Endowment plan — sum assured plus accumulated bonuses; typically 4–6% CAGR.

Death benefit:

Both — nominee receives the sum assured.

Flexibility:

Term insurance — high; cover and term can be chosen freely; riders added as needed.

Endowment plan — low; premiums are fixed and the product structure is rigid.

Returns:

Term insurance — no financial return; the "return" is protection itself.

Endowment plan — 4–6% CAGR, lower than PPF (7.1%), FDs (6–7%), and significantly below equity mutual funds over the long term.

Tax benefit:

Both — premiums qualify for deduction under Section 80C up to ₹1.5 lakh; death and maturity proceeds are exempt under Section 10(10D), subject to conditions.

Surrender:

Term insurance — no surrender value; you simply stop paying and the cover ends.

Endowment plan — surrender value available; from 2025, refund now accessible after just one year of premiums paid.

Best suited for:

Term insurance — anyone with dependents, liabilities (home loan, education loans), or income that others rely on.

Endowment plan — highly conservative individuals who want completely predictable, guaranteed (if low) returns and do not mind the lower cover.

Who Should Buy Term Insurance?

Term insurance is the right choice for the vast majority of earning individuals in India. If any of the following apply to you, a term plan should be the foundation of your financial protection:

- You have dependents — a spouse, children, or parents — whose financial life would be disrupted by the loss of your income

- You have outstanding liabilities — a home loan, car loan, or any debt that would pass on as a burden

- You want maximum life cover at the lowest possible premium

- You are in your 20s or 30s and your family is still in the wealth-accumulation phase

- You prefer to keep your investments separate and choose where your money grows

At Techolic, the first conversation we have with any client on insurance is: do you have adequate term cover? Not because term insurance is our product to sell, but because without it, every other financial plan — SIP, mutual funds, retirement corpus — is built on an unprotected foundation.

Who Should Buy an Endowment Plan?

Endowment plans are not inherently bad products. They are simply mismatched for most people. There are situations where they make reasonable sense:

- You have a highly conservative financial personality and cannot sleep at night without a guaranteed maturity payout — even if that payout underperforms other options

- You have no investment discipline and are likely to spend any savings you make rather than invest them — the forced lock-in of an endowment acts as a savings constraint

- You already have adequate term cover and are looking for a very small, guaranteed-return product as one component of a diversified plan

- You are planning for a specific near-term goal (5–10 years) and want capital protection above returns

If any of these describes you, an endowment plan can be a considered choice — not a default one.

Read: Best Term Life Insurance | Oros Life

Common Mistakes People Make When Choosing Between These Two

Treating "money back" as a reason to prefer endowment over term. The money you get back at maturity is not profit — it is your own premiums returned with a modest accumulation. When you account for inflation, the real value of that maturity amount is considerably lower than the nominal figure.

Buying endowment because the agent recommended it. First-year agent commission on endowment plans can be 25–40% of the premium. On a ₹4 lakh annual premium, that's up to ₹1.6 lakh in commission in year one alone. This creates a significant incentive mismatch between what's good for you and what gets recommended.

Assuming term insurance is only for old age. Term insurance is cheapest and most valuable when bought young. A 25-year-old pays a fraction of what a 45-year-old pays for the same cover. Every year you delay buying term insurance is a year of lower premiums you give up permanently.

Buying inadequate cover to keep the premium low. A ₹25 lakh sum assured on a term plan sounds better than nothing, but it doesn't replace even one year of a ₹6 lakh annual income. Cover should be sized at 15–20 times annual income — not at whatever premium feels comfortable.

Surrendering an endowment plan early without calculating the loss. If you already have an endowment plan and are considering surrendering it, the decision depends on how many years are remaining. In early years (1–3), you'll recover 30–50% of premiums.

Near maturity (final 2–3 years), it usually makes more sense to continue. The new IRDAI surrender value rules make early exit more viable than before, but it still warrants a proper calculation before acting.

The Smarter Strategy for Most Indian Families

Separate protection from investment. Always.

Buy a pure term plan sized at 15–20 times your annual income. Pay a fraction of what an endowment plan would cost. Take the remaining amount — the difference between what an endowment plan would have charged and what your term plan costs — and invest it in instruments suited to your actual goals:

SIPs for long-term wealth creation, PPF or NPS for retirement, and debt funds for medium-term goals.

This approach gives you better protection, better returns, and full flexibility — with no single product trying to do two jobs at once.

At Techolic, this is the framework we use when building insurance and investment plans for clients — term insurance as the foundation, goal-based investments on top.

If you are unsure whether your current insurance coverage is adequate or are wondering whether your endowment plan is actually working for you, our advisory team can review your portfolio and give you a clear, honest picture.

Frequently Asked Questions

1. Is term insurance better than an endowment plan?

For most people, yes. Term insurance gives significantly higher life cover at a fraction of the premium, and when the savings are invested separately, the long-term wealth created far exceeds endowment plan maturity values. Endowment plans work for very conservative investors who need guaranteed, predictable returns and are willing to accept lower cover and lower returns in exchange.

2. Do I get money back if I survive a term insurance policy?

Standard term insurance has no maturity benefit — if you survive the term, you receive nothing back. Some insurers offer a Return of Premium (ROP) variant that refunds premiums at maturity, but these cost significantly more (typically 50–100% higher premium) and still do not generate meaningful returns compared to investing the difference.

3. Are term insurance and endowment plan premiums tax-deductible?

Yes. Premiums paid for both term insurance and endowment plans qualify for deduction under Section 80C of the Income Tax Act, up to ₹1.5 lakh per year. Maturity and death benefit proceeds are also exempt under Section 10(10D), subject to the sum assured being at least 10 times the annual premium.

4. Is GST applicable on term insurance in India?

No. From September 22, 2025, individual life insurance premiums — including term plans and endowment plans — are exempt from GST. This makes both products marginally more affordable than they were before this change.

5. What happens if I stop paying premiums on an endowment plan?

If you stop paying premiums after the policy has acquired a surrender value (typically after 2–3 years under most policies), it converts to a paid-up policy with a reduced sum assured rather than lapsing entirely. Under the new IRDAI Special Surrender Value rules effective 2025, you can also now surrender and receive a refund after paying just one year of premiums.

6. How much term insurance cover do I actually need?

A widely used guideline is 15–20 times your annual income, with outstanding liabilities added on top. For example, if your annual income is ₹8 lakh and you have a ₹40 lakh home loan, your cover should be at minimum ₹1.6 crore (20x income) plus ₹40 lakh for the loan — so at least ₹2 crore in total.

7. Can I have both a term plan and an endowment plan?

Yes. There is no restriction on holding both. If you already have an endowment plan and need additional life cover, buying a term plan alongside is a practical way to bridge the gap in protection without surrendering the endowment mid-way and incurring surrender losses.