Mastering the Basics: A Guide to Understanding T-Accounts

Like any language, accounting has its own rules and structure and is occasionally known as the language of business. The T-account is an important element that is used in accounting. A straightforward-looking yet strong instrument for understanding how transactions affect a company's financial position is the T-account.

This article will make sure that you have a proper understanding of the T account and how it works. This will allow you to understand the nature of double-entry accounting with ease. What is a T-Account?

Introduction to T-Accounts

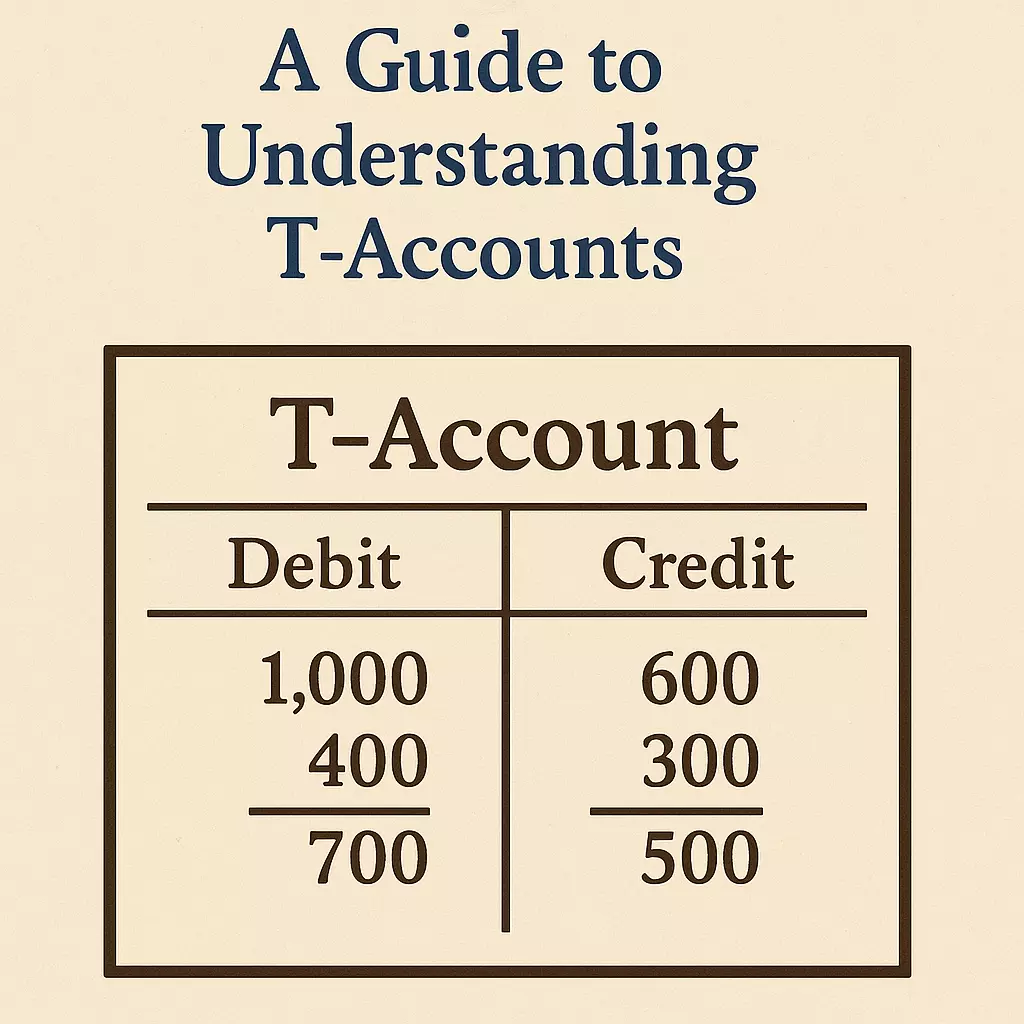

Visually represented by a T-account is a general ledger account. The form of the letter "T" gives it its name. The name of the account—like Cash or Accounts Payable—is listed at the absolute top of the "T". Debits are recorded on the left side of the T; credits are recorded on the right.

This structure lets students and accountants track how transactions change every account.

The left (debit) side of the Cash account, for example, would show a company receiving cash. Spending by the company will cause the amount to be on the right (credit) side. The simple left-and-right arrangement helps to properly register

transactions.

The Principle of Double-Entry Accounting

Double-entry accounting holds that every financial transaction affects at least two accounts. T-accounts help to fit within this bigger framework. It is a rule known to every human that every debit has an equal credit, and the T account is used to establish the same. This guarantees that the accounting equation—Assets = Liabilities + Equity—is always in balance.

Take a look at this T account example to understand how double-entry accounting is used for the same. Consider a business that buys furniture worth ₹20,000 in cash, for instance. Rising will cause the Furniture account, an asset, to be debited. Since its value will decrease, the Cash account, which is also an asset, will be debited. This transaction helps two accounts; it helps to remain in equilibrium.

Normal Balances and Account Types

Knowing how several accounts react in a T-account is vital. Generally speaking, asset accounts have a debit balance, which means that increases are reflected on the left side. Liability and equity accounts, on the other hand, have credit balances; therefore, gains are seen on the right.

Furthermore, increasing expense accounts are debit entries, and increasing revenue accounts are credit entries. A credit in the Service Revenue account and a debit in the Cash account would be recorded, say, by a firm producing ₹50,000 from a service. Both a rise in cash and a rise in income reflect the upkeep of the double-entry system.

Using T-Accounts for Analysis

T-accounts prove to be quite useful in trying to assess or correct entries. If you're not sure where an error happened in a ledger entry or journal, drawing out T-accounts can help you see the flow of cash. Finding mistakes is made much easier by it. For pupils and novices, these entries are a valuable learning tool as they assist them in grasping the justification of every entry before progressing to more advanced accounting techniques.

Moreover, T-accounts break down complex transactions into smaller pieces, therefore simplifying them. For instance, if a business obtained a bank loan for Rs 1,00,000, the Cash account would be debited and the Loan Payable account would be credited. Presented in a T-account shape, the effects of the transaction are easier to grasp.

Limitations on T-Accounts

Companies need accounting software to automate journal entries, ledgers, and financial statements as their business grows and transactions become more frequent. Still, a strong understanding of T-accounts is vital as the ideas behind them are the same ones accounting software utilises in the background.

T-accounts are hard to employ while trying to represent a large volume of transactions, which is yet another disadvantage. Simpler to handle and more succinct for regular business accounting are journal entries and ledger designs.

Conclusion

Accounting is built upon T-accounts. They offer a straightforward and lucid explanation of how transactions impact different accounts and how the dual nature of accounting maintains the balance of the financial records.

Even if their practical application in big operations may be restricted, the knowledge they provide is crucial for anyone studying accounting. Learning the concept of T-accounts is a step towards understanding the financial vocabulary of business, regardless of whether you are a student or the owner of a small company.