How UAV Parachute Recovery Systems Are Transforming Drone Safety

Introduction to UAV Parachute Recovery Systems

Definition and Operational Framework

Unmanned Aerial Vehicle (UAV) parachute recovery systems market industry represent an indispensable safeguard mechanism engineered to minimize the consequences of aerial malfunction, operational anomalies, or catastrophic failure.

These systems deploy parachutes either autonomously or manually to decelerate a drone during uncontrolled descent, thereby reducing kinetic impact energy and preserving both payload integrity and public safety.

Modern recovery architectures incorporate pyrotechnic launchers, compressed spring ejection assemblies, ballistic deployment modules, and intelligent flight-control integration.

Sophisticated variants can detect abnormalities such as power interruption, propeller malfunction, GPS signal loss, or sudden trajectory deviation. Upon detection, the parachute deploys within milliseconds.

What once served primarily military reconnaissance drones has now permeated commercial ecosystems.

Today, delivery drones, aerial cinematography units, agricultural UAVs, and infrastructure inspection platforms increasingly rely upon these systems as a prerequisite for operational continuity.

Importance in Unmanned Aerial Vehicle Safety

Drone traffic has proliferated dramatically over the past decade. As aerial density intensifies, safety expectations have evolved in parallel. UAV parachute recovery systems now function as a critical risk-mitigation apparatus within increasingly congested airspace.

Governments and aviation authorities across multiple jurisdictions have tightened operational regulations for beyond visual line of sight (BVLOS) missions and urban drone operations. In many cases, parachute recovery capabilities are becoming mandatory for drones operating above populated areas.

The rationale is straightforward. Mechanical failure at altitude can transform a lightweight UAV into a hazardous projectile. Even compact drones possess sufficient momentum to cause severe injury or infrastructural damage upon impact. Recovery systems reduce descent velocity substantially, transforming potential disasters into manageable incidents.

Insurance providers have also begun integrating parachute requirements into commercial drone liability frameworks. Consequently, recovery systems are no longer perceived merely as optional accessories; they are increasingly viewed as operational necessities.

Evolution of Recovery Technologies

Early UAV recovery mechanisms were rudimentary and mechanically constrained. Traditional systems relied upon manual deployment and suffered from delayed response intervals. Their operational reliability was inconsistent, particularly during high-speed flight or turbulent atmospheric conditions.

Contemporary solutions are markedly more advanced. Integrated avionics, machine learning algorithms, and sensor fusion technologies now enable predictive failure detection. Instead of reacting solely to catastrophic malfunction, advanced systems anticipate instability before total failure occurs.

Miniaturization has further accelerated adoption. Earlier parachute assemblies added substantial weight, thereby reducing payload efficiency and flight endurance. New-generation lightweight materials — including aramid fibers, ultra-high molecular weight polyethylene, and advanced composites — have drastically improved deployment efficiency without burdening aircraft performance.

The transformation reflects a broader industry trajectory toward intelligent aerial autonomy.

Market Dynamics Shaping Industry Expansion

Rising Adoption of Commercial Drones

Commercial drone adoption constitutes one of the strongest catalysts fueling the UAV parachute recovery systems market. Enterprises across logistics, mining, agriculture, telecommunications, and emergency response increasingly utilize drones for operational optimization.

E-commerce conglomerates are actively experimenting with autonomous aerial delivery ecosystems. Simultaneously, utility companies employ drones for power-line inspections, while agricultural firms use them for crop surveillance and pesticide dispersion. Each application expands operational exposure and elevates safety imperatives.

As commercial deployments multiply, the probability of midair malfunction correspondingly increases. Businesses seek to mitigate reputational, legal, and financial liabilities associated with drone incidents. Consequently, parachute recovery integration has emerged as a strategic investment rather than a discretionary expenditure.

Regulatory Mandates and Aviation Compliance

Regulatory institutions wield enormous influence over market acceleration. Aviation authorities worldwide are progressively refining drone safety standards, especially for operations conducted in urban environments or near critical infrastructure.

Several jurisdictions now require drones exceeding certain weight thresholds to incorporate fail-safe mechanisms. Parachute systems are frequently recognized as compliant solutions capable of satisfying operational safety criteria.

These mandates are particularly influential within sectors involving autonomous package delivery and passenger-adjacent airspace operations. Regulatory acceptance often determines whether commercial drone programs can scale beyond pilot projects.

The interplay between regulation and innovation creates a cyclical growth mechanism. As authorities demand greater safety compliance, manufacturers intensify research efforts, resulting in more reliable and affordable systems.

Technological Advancements in Autonomous Recovery Systems

Technological innovation continues reshaping competitive dynamics within the industry. Artificial intelligence, edge computing, inertial sensing, and predictive analytics are redefining how recovery systems function.

Advanced recovery modules can now communicate directly with onboard flight controllers. If abnormal behavior emerges, the system can execute pre-programmed emergency protocols before catastrophic descent occurs.

Some next-generation systems integrate geofencing intelligence, allowing parachute deployment strategies to adapt dynamically according to population density or terrain conditions. This contextual awareness enhances operational safety while minimizing collateral risk.

Battery efficiency improvements and low-power electronics have further enhanced system viability for smaller drones. As component costs decline, mass-market integration becomes increasingly achievable.

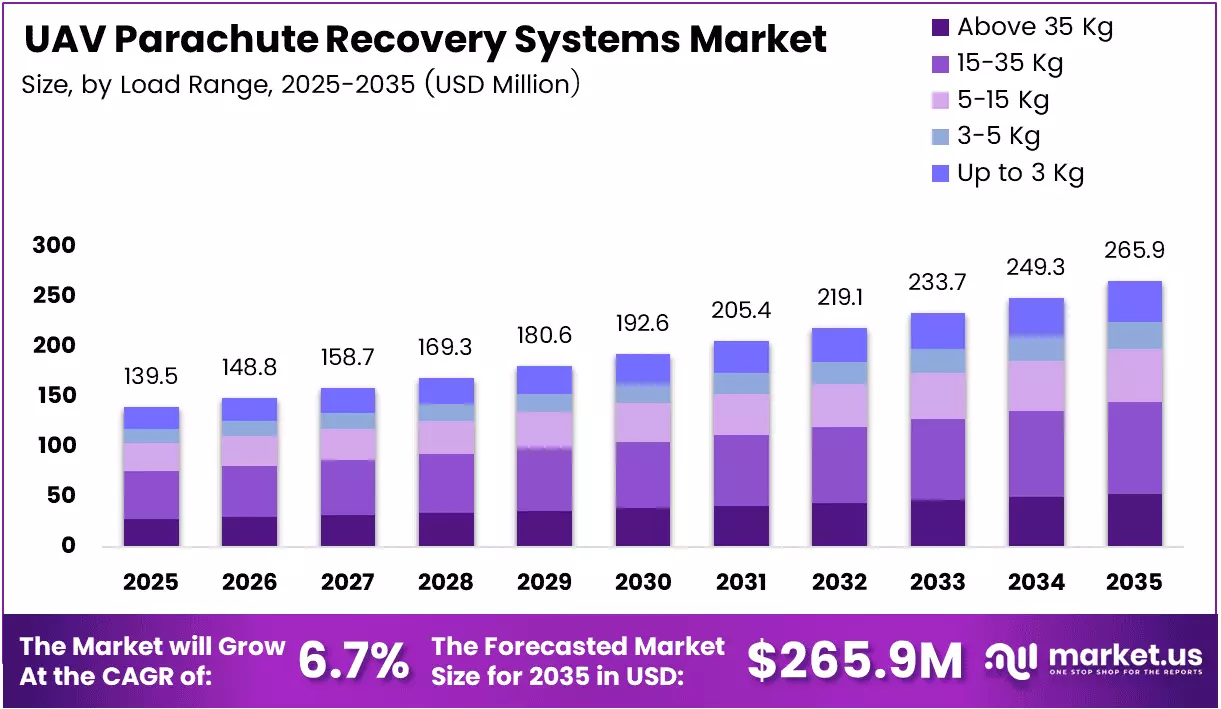

Key Market Segments

Fixed-Wing UAV Parachute Systems

Fixed-wing drones often operate at higher altitudes and velocities than rotary-wing alternatives. Consequently, their recovery systems require robust aerodynamic stabilization and rapid deployment capability.

These systems are extensively utilized in military reconnaissance, environmental mapping, and long-range surveillance missions. Due to their operational scale and investment value, fixed-wing platforms frequently incorporate premium-grade recovery technologies.

Ballistic parachute systems dominate this segment because they provide near-instantaneous deployment during emergencies. Their reliability under high-speed conditions makes them particularly valuable for large UAVs operating across extended flight corridors.

Rotary-Wing UAV Recovery Mechanisms

Rotary-wing drones, including quadcopters and hexacopters, represent the most commercially ubiquitous UAV category. Their applications range from filmmaking and surveying to parcel delivery and infrastructure monitoring.

Parachute systems designed for these drones emphasize compactness and low weight. Since many rotary-wing UAVs operate within dense urban environments, rapid deployment and precision descent are critically important.

This segment is experiencing rapid growth due to escalating consumer and enterprise drone adoption. Manufacturers increasingly bundle recovery systems as integrated safety features within premium commercial drone platforms.

Military Versus Commercial Applications

Military applications historically dominated the UAV parachute recovery market. Defense agencies required reliable recovery mechanisms to preserve expensive surveillance assets operating in hostile or inaccessible environments.

However, commercial demand is expanding at a significantly faster pace. Civilian industries now account for a growing proportion of total installations due to the explosion of drone-enabled services.

Commercial applications include:

- Logistics and delivery

- Precision agriculture

- Construction surveying

- Emergency response

- Cinematography

- Telecommunications inspection

Military demand remains substantial, especially for tactical drones and intelligence platforms, yet commercial diversification is reshaping overall market structure.

OEM and Aftermarket Installations

Original Equipment Manufacturer (OEM) installations are becoming increasingly prevalent as drone manufacturers integrate recovery systems during production. This approach improves compatibility, reduces installation complexity, and enhances regulatory compliance.

Aftermarket installations remain relevant for legacy drone fleets and specialized industrial operations. Numerous operators retrofit existing UAVs to meet updated aviation regulations or insurance requirements.

The OEM segment is expected to witness accelerated growth due to seamless integration advantages and growing institutional emphasis on certified safety architectures.

Regional Market Analysis

North American Market Leadership

North America remains the dominant regional market due to its mature drone ecosystem, advanced aerospace infrastructure, and progressive regulatory environment.

The United States, in particular, has witnessed substantial investment in commercial drone logistics and defense modernization initiatives. Regulatory frameworks encouraging BVLOS testing have further stimulated demand for advanced recovery technologies.

The presence of prominent aerospace innovators and drone manufacturers strengthens regional market leadership.

European Regulatory Influence

Europe exerts considerable influence through stringent aviation safety regulations and proactive drone governance frameworks. The region emphasizes operational accountability, particularly in urban environments.

Countries such as Germany, France, and the United Kingdom have accelerated certification requirements for commercial UAV operations. These policies encourage widespread adoption of parachute recovery systems.

European manufacturers are also investing heavily in environmentally sustainable materials and energy-efficient deployment mechanisms.

Asia-Pacific Growth Trajectory

Asia-Pacific is emerging as the fastest-growing regional market. Rapid industrialization, expanding e-commerce activity, and government-backed drone initiatives contribute significantly to market momentum.

China plays a pivotal role due to its dominant position in drone manufacturing. Simultaneously, India, Japan, and South Korea are expanding drone applications across agriculture, logistics, and disaster management.

As regional regulations mature, safety compliance adoption is expected to intensify considerably.

Emerging Opportunities in the Middle East and Latin America

The Middle East and Latin America present nascent yet promising growth opportunities. Infrastructure inspection, oil and gas surveillance, and border monitoring applications are expanding across these regions.

Governments increasingly recognize drones as cost-efficient tools for environmental observation and public security. Consequently, demand for reliable recovery systems is anticipated to strengthen steadily over the coming decade.

Read: Best Homework Help Platforms for Multidisciplinary Students

Competitive Landscape and Industry Participants

Major Manufacturers and Innovators

The market comprises specialized aerospace firms, defense contractors, and emerging drone safety startups. Competition revolves around reliability, deployment speed, weight optimization, and regulatory certification.

Manufacturers increasingly differentiate themselves through proprietary algorithms capable of ultra-fast anomaly detection and autonomous activation.

Strategic Collaborations and Acquisitions

Strategic alliances have become commonplace as drone manufacturers collaborate with parachute technology providers to accelerate certification processes and improve interoperability.

Acquisitions are also reshaping the competitive environment. Larger aerospace corporations frequently acquire innovative startups to consolidate technological capabilities and expand product portfolios.

This consolidation trend may intensify as the industry matures.

Research and Development Initiatives

Research activity remains vigorous across multiple technological domains, including:

- AI-assisted deployment analytics

- Smart textile engineering

- Lightweight propulsion-safe ejection systems

- Redundant sensor architectures

- Predictive maintenance diagnostics

Companies capable of achieving superior reliability with minimal weight penalties are likely to secure substantial competitive advantages.

Challenges and Constraints

High Integration and Maintenance Costs

Despite growing adoption, cost remains a considerable barrier. High-performance parachute systems require advanced sensors, deployment mechanisms, and software integration.

For small-scale drone operators, installation expenses may appear disproportionate relative to aircraft value. Maintenance and certification costs further compound operational expenditures.

Payload Limitations and Deployment Complexities

Parachute assemblies inevitably consume payload capacity. For lightweight drones, even modest weight additions can significantly reduce endurance and maneuverability.

Deployment complexity also presents engineering challenges. Incorrect parachute deployment timing or entanglement with propellers can compromise recovery effectiveness.

Manufacturers continue striving to optimize compactness while preserving deployment reliability.

Reliability Concerns Under Adverse Conditions

Environmental variables remain problematic. High winds, rain, electromagnetic interference, and extreme temperatures can impair deployment performance.

Operational consistency under unpredictable atmospheric conditions remains an ongoing engineering challenge. Reliability certification standards are therefore becoming increasingly rigorous.

Future Trends and Emerging Opportunities

AI-Enabled Recovery Systems

Artificial intelligence is expected to become a transformative force within UAV recovery architectures. AI-driven analytics can identify subtle flight irregularities invisible to traditional systems.

These capabilities may eventually enable predictive emergency response rather than reactive deployment alone.

Lightweight Composite Parachute Materials

Material science innovation is accelerating rapidly. Ultralight fabrics with exceptional tensile strength are improving deployment efficiency while minimizing payload penalties.

Future parachutes may incorporate adaptive aerodynamic structures capable of dynamically adjusting descent behavior during flight.

Integration with Urban Air Mobility Ecosystems

Urban air mobility represents a frontier opportunity for the industry. As autonomous aerial taxis and advanced drone corridors emerge, safety systems will become indispensable infrastructure components.

Parachute recovery technologies may evolve into standardized compliance requirements for urban airspace certification.

Expansion of Drone Logistics Networks

Global logistics networks increasingly depend upon autonomous delivery drones for rapid distribution efficiency. This evolution substantially enlarges the addressable market for recovery systems.

Every additional drone operating above populated environments increases demand for dependable fail-safe technologies. Consequently, parachute recovery integration is poised to become ubiquitous across commercial fleets.

Conclusion

The UAV parachute recovery systems market is transitioning from a niche aerospace specialty into a foundational pillar of drone safety infrastructure. Accelerating commercial drone adoption, intensifying regulatory oversight, and continuous technological innovation are collectively propelling industry expansion.

Although challenges related to cost, payload efficiency, and environmental reliability persist, ongoing advancements in artificial intelligence, material engineering, and autonomous flight systems are steadily overcoming these limitations.

The future trajectory appears exceptionally promising. As drones become deeply embedded within logistics, surveillance, agriculture, emergency response, and urban mobility ecosystems, parachute recovery systems will assume an increasingly central role in safeguarding aerial operations.

In an era defined by autonomous aviation proliferation, safety is no longer peripheral. It is the architecture upon which the future of unmanned flight will ultimately be built.