Features of Modern Loan Origination Software: The Complete Guide for NBFCs & Banks

The financial lending landscape in India has undergone a seismic shift over the last decade. Gone are the days when loan applications involved mountains of paperwork, lengthy in-branch queues, and weeks-long approval timelines.

Today, borrowers expect instant decisions, seamless digital journeys, and frictionless disbursals — and lenders who cannot deliver this experience risk losing customers to faster, more agile competitors.

At the heart of this transformation lies Loan Origination Software (LOS) — the technological backbone that powers a lender's ability to accept, evaluate, approve, and disburse loans with speed, accuracy, and compliance.

But not all loan origination systems are built equal. Modern LOS platforms have evolved far beyond simple application trackers into intelligent, integrated, AI-driven ecosystems.

In this guide, we break down the essential features of modern loan origination software, explain why each feature matters, and show how platforms like Roopya are redefining what lending infrastructure looks like for NBFCs, banks, MFIs, and fintech lenders in India.

What Is Loan Origination Software?

Loan Origination Software (LOS) is a digital platform that manages the complete lifecycle of a loan from the moment a borrower submits an application to the point of loan disbursement.

It orchestrates every step in between — identity verification, creditworthiness assessment, document collection, underwriting, approval workflows, and sanction — in a structured, automated, and auditable manner.

For lenders, a robust LOS is not just a convenience tool; it is a competitive necessity. According to industry research, lenders using modern LOS platforms process loans up to 10x faster than those relying on manual or legacy systems, while also dramatically reducing processing costs and default rates.

Top Features of Modern Loan Origination Software

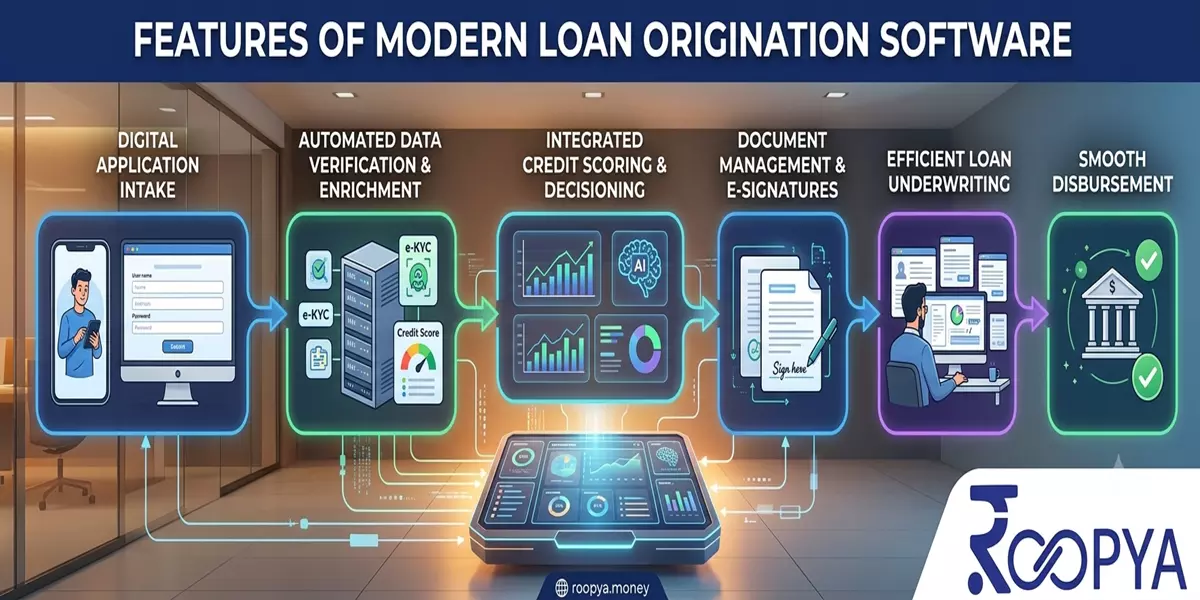

1. Digital Application & Fully Paperless Onboarding

The first touchpoint in any lending journey is the application. Modern LOS platforms offer fully digital, mobile-first application interfaces that allow borrowers to apply for loans from anywhere — no branch visit required. These platforms support dynamic forms that adapt based on loan product type, borrower profile, and regulatory requirements.

Key capabilities include:

- Multi-device application forms (mobile, tablet, desktop)

- Dynamic field rendering based on borrower type (salaried, self-employed, business)

- Real-time field validation to reduce data entry errors

- Auto-fill from Aadhaar, PAN, or bank statement data

- Support for 20+ pre-configured loan products out of the box

Roopya's platform, for instance, enables lenders to go live with fully configured digital loan journeys in as little as 1 day — without writing a single line of code.

2. Automated KYC & Document Verification

Manual document verification is not just slow — it is expensive, error-prone, and a major bottleneck in the loan origination funnel. Modern LOS platforms integrate automated KYC (Know Your Customer) workflows that verify borrower identity documents instantly using AI-powered OCR (Optical Character Recognition) and NLP (Natural Language Processing).

What automated KYC covers:

- Aadhaar-based e-KYC and Video KYC (V-KYC)

- PAN card validation and NSDL/UTIITSL integration

- Face match and liveness detection

- Bank statement analysis and parsing

- GST return and ITR document parsing for business loans

- Real-time fraud flag detection on uploaded documents

Platforms like Roopya process document verification with 99%+ accuracy, reducing turnaround time from hours to seconds while maintaining full RBI compliance.

3. No-Code Business Rule Engine (BRE)

A Business Rule Engine is the decision-making brain of your LOS. It is where credit policies come to life — determining which applications are approved, rejected, or referred for manual review based on pre-defined rules and thresholds.

What distinguishes a modern BRE from legacy rule systems is its no-code, visual interface. Credit teams can configure, modify, and deploy complex multi-layered lending rules — without needing IT involvement or code deployments.

Features of a modern no-code BRE:

- Drag-and-drop rule builder with visual logic trees

- Support for 100+ rule parameters (bureau scores, income, vintage, sector, geography)

- Multi-level rule cascading with AND/OR logic

- A/B testing of different rule versions

- Self-learning capabilities through ML-based pattern recognition

- Auto-optimization of rules based on historical approval and default data

Roopya's BRE is self-configurable by business users, giving lenders full autonomy to adapt credit policies to changing market conditions — instantly and without downtime.

4. Intelligent Credit Scoring & Decisioning

Traditional credit assessment relied almost entirely on bureau scores from agencies like CIBIL, Experian, or Equifax. While bureau data remains important, it excludes a significant segment of India's population — the thin-file or new-to-credit borrowers.

Modern LOS platforms supplement bureau data with alternative data sources and machine learning models to enable more accurate, inclusive credit decisions.

What intelligent credit decisioning includes:

- Real-time bureau pulls from CIBIL, Experian, Equifax, and CRIF

- Alternative data scoring using bank transactions, UPI patterns, and GST data

- Behavioral data analysis from digital footprint

- ML-based probability of default (PD) modelling

- Custom application scorecard development

- Real-time credit decisions in milliseconds

Roopya's AI-powered credit decisioning evaluates thousands of data points simultaneously, delivering 40% better accuracy compared to traditional single-bureau scoring methods.

5. 300+ Pre-Integrated APIs

A loan origination system does not operate in isolation. It needs to communicate with a vast ecosystem of third-party services — credit bureaus, bank statement analyzers, payment gateways, e-sign providers, digital lockers, and regulatory platforms. Manually integrating each of these is time-consuming, expensive, and technically complex.

Modern LOS platforms come with pre-integrated API libraries that connect lenders to the entire fintech ecosystem on day one. This dramatically reduces time-to-market and integration costs.

Categories covered by pre-integrated APIs:

- Credit bureau integrations (CIBIL, Experian, Equifax, CRIF)

- KYC providers (Aadhaar, DigiLocker, NSDL, Video KYC vendors)

- Bank statement analyzers (Finvu, Perfios, OneMoney)

- Payment gateways and NACH mandate registration

- E-sign and digital agreement platforms

- GST and income tax verification APIs

- Fraud detection and device intelligence APIs

Roopya offers 300+ pre-integrated APIs, giving lenders a complete integration ecosystem without the burden of individual vendor negotiations or technical integration work.

6. AI-Powered Fraud Detection

Loan fraud is a growing challenge for lenders in India, with synthetic identity fraud, document forgery, and application fraud causing billions in losses annually. Modern loan origination software embeds AI-powered fraud detection modules that analyse every application in real time for suspicious signals.

Fraud detection capabilities in modern LOS:

- Duplicate application detection across borrower identity markers

- Document tampering and forgery detection using image forensics

- Device fingerprinting and IP intelligence

- Behavioural biometric analysis during application completion

- Name and address mismatch detection

- Blacklist screening against internal and external fraud registries

Roopya's built-in AI fraud modules have helped lenders reduce fraud exposure by up to 80%, making fraud prevention a first-class citizen of the origination process rather than an afterthought.

7. Configurable Loan Approval Workflows

Different loan products, ticket sizes, and borrower segments require different approval processes. A personal loan under ₹50,000 may qualify for straight-through processing (STP) with no human involvement, while a ₹2 crore SME loan may require multi-level underwriter review, legal checks, and credit committee sign-off.

Modern LOS platforms support highly configurable multi-stage approval workflows that can be tailored for each loan product:

- Role-based access for underwriters, credit officers, and branch managers

- Parallel and sequential approval stages

- SLA-based escalation triggers

- Maker-checker controls for large-value loans

- Digital credit memo generation

- One-click sanction letter generation and digital delivery

8. E-Sign & Digital Agreement Management

Wet ink signatures on physical loan agreements are an anachronism in digital lending. Modern LOS platforms integrate legally valid Aadhaar-based e-sign and eStamp facilities that allow borrowers to digitally sign loan agreements from anywhere — on their mobile phone, within seconds.

This capability includes:

- Aadhaar OTP-based e-signature (legally valid under the IT Act, 2000)

- Automated loan agreement generation from configurable templates

- eStamp duty integration for applicable states

- Secure document vault for storing signed agreements

- Audit trail for every signing event

9. Real-Time Loan Tracking & Borrower Communication

Borrowers want visibility into their loan application status at every stage. Modern LOS platforms provide real-time application tracking via borrower portals and automated communication workflows that keep borrowers informed via SMS, email, and WhatsApp — without requiring any manual intervention from the lender's team.

Communication capabilities include:

- Automated status updates at each workflow stage

- WhatsApp, SMS, and email notification triggers

- Borrower self-service portal for document uploads and status checks

- In-app chat support integration

- Configurable communication templates by loan product and stage

Read: Top Software Companies in 2026: Industry Leaders Driving

10. Comprehensive Reporting & Lending Analytics

Data is the lifeblood of a modern lending business. Modern LOS platforms offer built-in analytics and reporting capabilities that give lenders real-time visibility into every aspect of their origination funnel — from application volumes and approval rates to processing times and rejection reasons.

Reporting capabilities in modern LOS:

- Real-time origination dashboards for management

- Funnel analytics showing drop-off at each stage

- Credit officer productivity reports

- Regulatory and RBI reporting templates

- Custom report builder with export to Excel/PDF

- AI-generated narrative insights from portfolio data

Roopya's lending analytics module uses natural language processing to allow lenders to ask questions about their portfolio in plain English and receive instant, AI-generated insights — saving hours of manual report preparation.

11. Open API Architecture & Seamless Integrations

A modern LOS must integrate seamlessly with the broader technology stack a lender already uses — CRMs, ERPs, core banking systems, collections platforms, and data warehouses. Open API architecture ensures that the LOS can communicate bidirectionally with any system that supports REST APIs.

Integration capabilities:

- RESTful APIs for every core origination function

- Webhook support for real-time event-driven integrations

- Native connectors for leading CRMs and ERPs

- Core banking system (CBS) integration for post-sanction handoff

- Data export compatibility with BI tools like Power BI and Tableau

12. Regulatory Compliance & Audit Trail

For NBFCs and banks operating under RBI oversight, regulatory compliance is non-negotiable. Modern LOS platforms are built with compliance at their core — continuously updated to reflect the latest RBI guidelines on digital lending, data localisation, fair practice codes, and KYC norms.

Compliance features include:

- Configurable loan agreement templates aligned with RBI fair practice code

- Complete audit trail for every decision made during origination

- Data residency controls ensuring data stays in India

- Role-based access control with comprehensive activity logging

- Integration with RBI reporting frameworks

- Automated alerts for regulatory threshold breaches

Why Roopya Is the Right Loan Origination Software for Indian Lenders

Roopya is a next-generation, no-code unified lending infrastructure platform purpose-built for NBFCs, banks, MFIs, and modern fintech lenders in India. Unlike legacy LOS vendors that require months of implementation and expensive IT resources, Roopya offers:

- Go-live in 1 day with plug-and-play lending infrastructure

- Zero upfront cost with a pay-as-you-use pricing model

- 20+ pre-configured loan products including personal, business, gold, home, auto, and payday loans

- 300+ pre-integrated APIs covering the full fintech ecosystem

- A truly no-code platform that empowers business users — not just developers

- Always-updated compliance aligned with the latest RBI regulations

- AI-powered document analysis, credit decisioning, fraud detection, and analytics

Trusted by modern lenders like IndiaKaLoan, QuickFinShop, Recapita, FindDoc, EazyCredit, and LoanSeva, Roopya has proven its ability to help lenders scale their lending operations efficiently — from origination through to collections.

Frequently Asked Questions (FAQs)

Q1. What is loan origination software?

Loan origination software (LOS) is a digital platform that automates and manages the end-to-end process of originating loans — from application submission and KYC verification to credit assessment, approval workflows, and loan disbursement. It replaces manual, paper-based processes with digital, automated workflows that are faster, more accurate, and more cost-efficient.

Q2. What are the key features to look for in a modern LOS?

The most important features in a modern loan origination system include: digital application forms, automated KYC and document verification, a no-code business rule engine, AI-powered credit decisioning, pre-integrated APIs (300+ in the case of Roopya), fraud detection, configurable approval workflows, e-sign capabilities, real-time borrower communication, and comprehensive compliance and reporting tools.

Q3. How is modern LOS software different from traditional loan processing systems?

Traditional loan processing systems are largely manual, siloed, and require significant IT involvement for any changes. Modern LOS platforms are cloud-native, no-code, AI-powered, and API-first. They offer real-time decisioning, deep third-party integrations, and self-service configuration for business users — dramatically reducing both time-to-market and operational costs.

Q4. How quickly can an NBFC go live with Roopya's loan origination platform?

Roopya is designed for rapid deployment. NBFCs and lenders can go live with their digital lending operations in as little as 1 day, thanks to Roopya's plug-and-play infrastructure, pre-configured loan products, and no-code setup process that requires zero technical expertise.

Q5. Does Roopya's LOS comply with RBI digital lending guidelines?

Yes. Roopya's platform is continuously updated to ensure full compliance with RBI's evolving regulatory framework, including digital lending guidelines, KYC norms, data localisation requirements, and fair practice codes. Lenders using Roopya benefit from always-current compliance without needing to manage regulatory changes themselves.

Q6. Can Roopya's loan origination software integrate with our existing core banking system?

Absolutely. Roopya is built on an open API architecture that supports seamless integration with core banking systems, CRMs, ERPs, and other business tools via REST APIs. This ensures that Roopya can function as the origination layer within a lender's existing technology ecosystem without disruption.

Q7. What types of loan products does Roopya's LOS support?

Roopya supports 20+ pre-configured loan products, including personal loans, business loans, SME loans, gold loans, home loans, auto loans, payday loans/salary advance products, and microfinance loans. Lenders can configure and launch any of these products without writing code.

Q8. How does AI improve the loan origination process?

AI enhances loan origination in multiple ways: it automates document analysis with near-perfect accuracy, enables real-time credit scoring using thousands of data points including alternative data, detects fraud patterns that rule-based systems miss, and generates predictive insights from portfolio data. Roopya's AI capabilities have helped lenders process applications 10x faster, improve credit accuracy by 40%, and reduce fraud by up to 80%.