Down Payment Bungalow Canada: A Realistic 2026 Guide for Buyers

Buying a bungalow in Canada in 2026 requires more than just saving a deposit. You need to understand how the down payment system works, what lenders expect, and the true cost of ownership.

This guide breaks everything down in simple terms so you can make informed decisions without surprises.

What Is the Minimum Down Payment in Canada 2026?

The minimum down payment in Canada depends on the purchase price of the home. It is not a flat percentage.

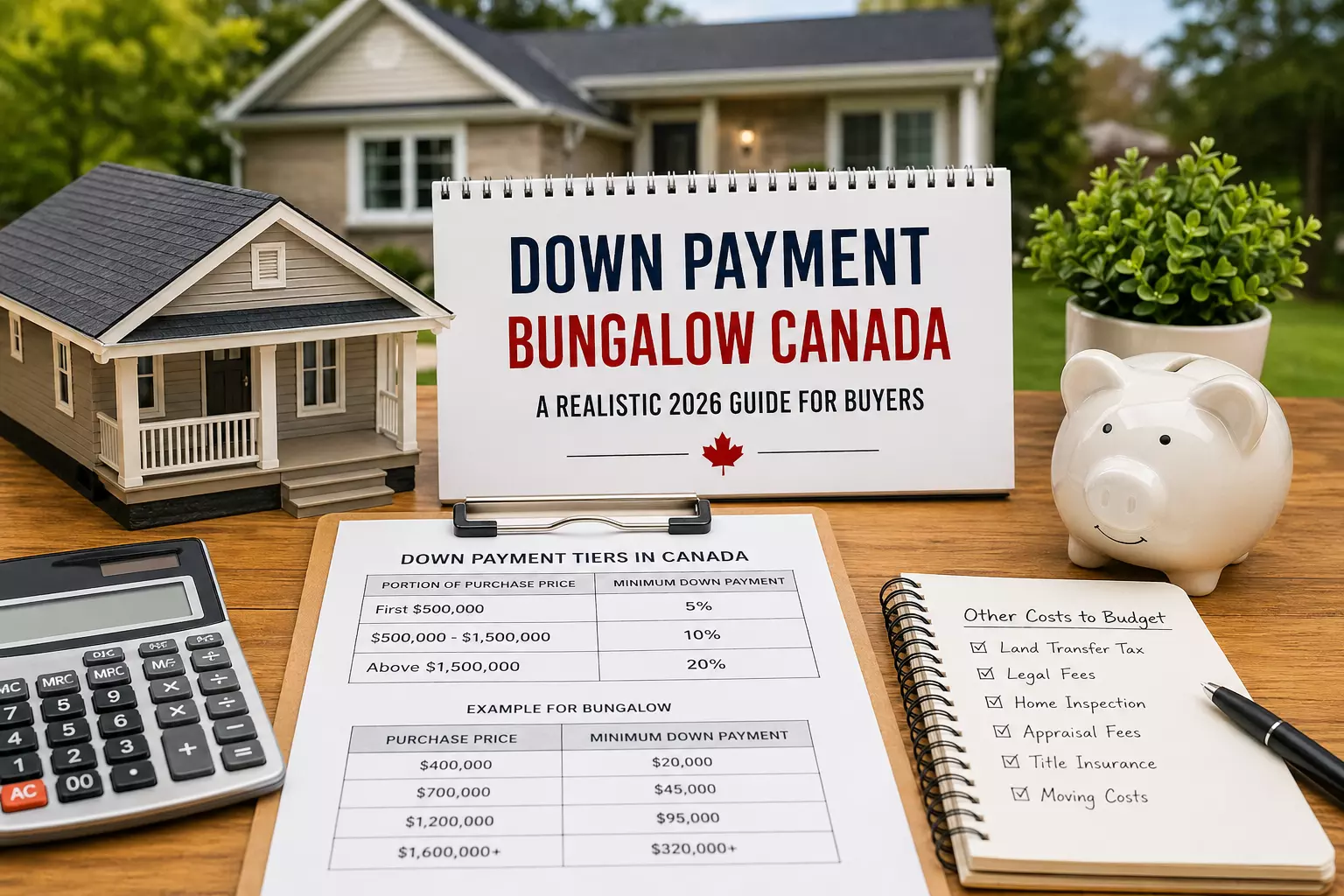

In 2026, the minimum down payment Canada 2026 rules follow a tiered system set by federal mortgage regulations. This means buyers must calculate their down payment based on price brackets rather than a single rate.

Canada Mortgage Down Payment Tiers Explained

Canada uses a structured system:

- 5% on the first $500,000

- 10% on the portion between $500,000 and $1,500,000

- 20% for homes priced above $1,500,000

These Canada mortgage down payment tiers are mandatory for insured and uninsured mortgages.

Important fact:

If your down payment is less than 20%, you must pay mortgage default insurance (often called CMHC insurance).

How Much Down Payment for Bungalow Ontario?

The answer depends entirely on the purchase price of the bungalow.

In markets like Ontario, bungalow prices vary widely. Smaller towns may still offer homes under $500,000, while urban areas often exceed $1 million.

Let’s look at realistic examples to understand how much down payment for bungalow Ontario.

Real Down Payment Examples for 2026

Example 1: $400,000 Bungalow

- 5% of $400,000 = $20,000

- This meets the minimum requirement

This is the simplest case under down payment bungalow Canada rules.

Example 2: $700,000 Bungalow

- 5% on first $500,000 = $25,000

- 10% on remaining $200,000 = $20,000

- Total down payment = $45,000

This is a common price point in suburban Ontario markets.

Example 3: $1.2 Million Bungalow

- 5% on first $500,000 = $25,000

- 10% on next $700,000 = $70,000

- Total down payment = $95,000

Still under $1.5 million, so less than 20% is allowed (but insurance applies).

Example 4: Above $1.5 Million

- Minimum 20% required

- Example: $1.6M home = $320,000 down payment

Key rule: Homes over $1.5 million are not eligible for insured mortgages.

What Are the Official Down Payment Rules Canada?

The down payment rules Canada are set by federal regulators and enforced by lenders.

Here are the core rules:

- Minimum 5% down for homes under $500,000

- Tiered structure for homes up to $1.5M

- Mandatory 20% down for homes above $1.5M

- Mortgage insurance required if down payment is under 20%

Fact: Mortgage insurance protects the lender, not the buyer, but it allows buyers to enter the market with smaller down payments.

What Mortgage Requirements Should Buyers Expect?

Saving a down payment is only part of the process. Lenders evaluate your financial profile carefully.

Do You Need to Pass the Stress Test?

Yes. All buyers must pass the mortgage stress test.

- You must qualify at a higher interest rate than your actual mortgage rate

- Typically, this is either the Bank of Canada benchmark rate or your contract rate + 2%

Fact: This rule ensures borrowers can handle future rate increases.

What Income and Credit Score Are Required?

Lenders assess:

- Stable income (employment or business)

- Debt-to-income ratio

- Credit score (usually 680+ preferred for best rates)

Fact: A higher credit score can reduce borrowing costs and improve approval chances.

What About CMHC Insurance?

If your down payment is less than 20%, mortgage insurance is required.

- Premium ranges roughly from 2.8% to 4% of the mortgage

- It can be added to your mortgage balance

Fact: This insurance is regulated and applies across Canada, not just Ontario.

What Are the Hidden Bungalow Purchase Costs Canada?

Many buyers underestimate bungalow purchase costs Canada beyond the down payment.

Here are the major closing costs in Ontario:

Land Transfer Tax

- Based on property value

- Ontario has both provincial and (in some cities) municipal tax

Fact: In Toronto, buyers pay double land transfer tax.

Legal Fees

- Typically $1,500 to $3,000

- Covers title transfer and legal paperwork

Home Inspection

- Usually $400 to $700

- Highly recommended for older bungalows

Appraisal Fees

- Around $300 to $600

- Required by lenders to confirm property value

Title Insurance

- One-time cost, usually $250 to $500

Total Closing Cost Estimate

Buyers should budget 1.5% to 4% of the purchase price for closing costs.

What First Time Home Buyer Down Payment Ontario Supports Exist?

First-time buyers in Ontario have access to several helpful programs.

RRSP Home Buyers’ Plan

- Allows withdrawal of up to $60,000 (2026 limit) from RRSP

- Funds must be repaid over 15 years

Fact: This is one of the most widely used programs for first-time buyers.

Land Transfer Tax Rebates

- Ontario rebate up to $4,000

- Additional rebate available in Toronto

First-Time Home Buyer Incentive (Status Note)

- This federal shared equity program has been phased out in recent years

- Buyers should confirm availability as policies evolve

What Are the Ongoing Costs After Buying a Bungalow?

Owning a bungalow comes with continuous expenses that go beyond your mortgage.

Monthly Costs to Expect

- Mortgage payments

- Property taxes

- Home insurance

- Utilities

- Maintenance and repairs

Why Full Affordability Matters

Buying at your maximum budget can create financial pressure.

Fact: Financial experts often recommend keeping total housing costs below 30–39% of gross income.

Maintenance Costs for Bungalows

Bungalows often sit on larger lots, which means:

- Higher maintenance costs

- Landscaping expenses

- Roof and foundation upkeep

Tip: Set aside 1% of home value annually for maintenance.

Read: Top 10 Emerging Trends in the Real Estate Market for 2025

Is It Better to Put 20% Down?

Putting 20% down eliminates mortgage insurance and reduces monthly payments.

However, it is not always necessary.

Pros of 20% Down

- No CMHC insurance

- Lower monthly payments

- Better mortgage terms

Cons

- Requires significantly more savings

- Delays entry into the housing market

Balanced view: Many buyers choose less than 20% to enter the market sooner.

Key 2026 Market Insights Buyers Should Know

- Interest rates remain a major affordability factor in 2026

- Bungalows often carry a price premium due to demand and limited supply

- Urban Ontario markets continue to see strong competition

- Smaller cities and rural areas offer more affordable entry points

Fact: Single-level homes are increasingly popular among retirees and downsizers, which drives demand.

FAQ: Down Payment Bungalow Canada

How much down payment is required for a bungalow in Canada?

It depends on the price. Minimum starts at 5%, but increases with price tiers and reaches 20% for homes above $1.5 million.

Can I buy a bungalow with 5% down in Ontario?

Yes, if the home price is under $500,000. For higher prices, tiered rules apply.

What is the minimum down payment Canada 2026 rule?

5% up to $500K, 10% on the portion up to $1.5M, and 20% beyond that.

Do first-time buyers need less down payment?

No special reduction in minimum percentage, but programs help with funding and tax rebates.

What is included in bungalow purchase costs Canada?

Costs include land transfer tax, legal fees, inspections, insurance, and other closing expenses.

Is mortgage insurance mandatory?

Yes, if your down payment is less than 20%.

Final Thoughts

Understanding the down payment bungalow Canada system in 2026 is essential before entering the market. The tiered structure, mortgage requirements, and hidden costs all play a role in determining affordability.

A realistic plan should include:

- Correct down payment calculation

- Full awareness of closing costs

- Strong financial preparation

Buying a bungalow is a major financial step. The more clarity you have at the start, the smoother the process becomes.