Compound Interest Calculator: See How Your Money Actually Grows

Why I Built This Tool

Let me be honest: I created this compound interest calculator for one simple reason - I wanted to know how much my monthly savings would be worth in 10 years.

The calculators out there were either too basic, ugly as hell, or packed with ads trying to sell me something. As a developer, I thought: if nothing satisfies me, why not build my own?

Turns out, this thing became pretty useful. Not only do I use it regularly, but friends started asking for the link too.

What Does This Tool Actually Do?

1. Shows You the Real Power of Dollar-Cost Averaging

The most common scenario: monthly index fund investing

Say you invest $500 every month in an index fund with 8% annual returns (roughly the S&P 500 long-term average). What happens after 10 years?

- Total invested: $60,000

- Final value: ~$91,500

- Pure profit: $31,500

That's compound interest in action. The first few years look boring, but the growth accelerates dramatically later on.

2. Compare Different Investment Strategies

The tool supports different contribution frequencies:

- $500 monthly vs $1,500 quarterly vs $6,000 annually

- Results vary slightly, but the difference isn't as big as you'd think

This taught me something important: starting to invest matters more than obsessing over the perfect frequency.

3. See How Inflation Eats Your Money

This feature is a real eye-opener.

Imagine having $100,000 in 10 years. Sounds like a lot, right? But with 3% annual inflation, that $100k has the purchasing power of about $74k today.

Money loses value - that's reality. Just keeping cash in savings accounts isn't enough. You need to beat inflation.

4. Set Realistic Financial Goals

Want to buy a house? A new car? Save for your kid's college?

Input your target amount and work backwards to see how much you need to invest monthly and what return rate you need. This turns vague dreams into actionable plans.

Real-World Usage Stories

Story 1: The Millennial's First Investment

My friend Jake, 28, makes $50k a year and can save $800 monthly. He was keeping everything in a high-yield savings account earning 2%.

We ran the numbers:

- Savings account (10 years): $96k invested, $106k final value

- Index fund investing (assuming 7% returns): $96k invested, $132k final value

- Difference: $26k

Result: Jake started his first investment account.

Story 2: Mid-Career Retirement Planning

My colleague Sarah, 35, wants $1 million for retirement at 65.

The calculation: With 6% annual returns, she needs to invest about $1,000 monthly for 30 years.

Sarah realized this was totally doable with her current income and started a systematic retirement investment plan.

Story 3: New Parent's College Fund

My neighbor Tom just had a baby and wants $200k for college in 18 years.

The math: With 7% annual returns, he needs to invest about $550 monthly.

Tom thought this was manageable and started a 529 college savings plan.

What Makes This Tool Different

1. Clean Interface, Simple Operation

Unlike bank calculators that are overly complex or apps that are flashy but useless. This is straightforward - input data, see results.

2. Accurate Calculations

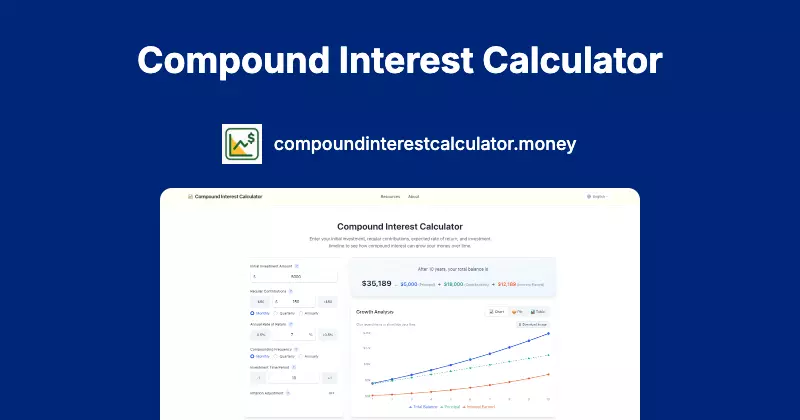

Uses standard compound interest formulas with support for different compounding frequencies (monthly, quarterly, annually).

3. Great Visualizations

Charts show your money's growth curve, making the "snowball effect" of compound interest visible.

4. Multiple Export Options

Download Excel spreadsheets or save chart images. Perfect for keeping investment records or showing family members.

5. Completely Free

No ads, no sales pitches, just a pure calculation tool.

Tips from Actually Using This Tool

1. Don't Be Overly Optimistic

Don't set return rates too high. The S&P 500 averages about 10% long-term, but that includes major ups and downs.

2. Factor in Inflation

Always turn on the "inflation adjustment" feature to see real purchasing power. This makes your goals more realistic.

3. Review Your Plan Annually

Use this tool every year to recalculate based on actual performance and adjust your contributions or expectations.

4. Don't Change Strategies Too Often

Compound interest needs time to work. Frequent changes can hurt your results.

Some Real Talk About Investing

Expected Returns by Risk Level

- Conservative: 4-6% annually (bonds, CDs, high-yield savings)

- Moderate: 6-8% annually (balanced funds, target-date funds)

- Aggressive: 8-12% annually (stock index funds, individual stocks)

Remember: higher returns = higher risk.

How Much to Invest

Consider the 50/30/20 rule:

- 50% for needs (rent, food, utilities)

- 30% for wants (entertainment, dining out)

- 20% for savings and investments

Investment Timeline

- Short-term goals (1-3 years): Keep it conservative

- Medium-term goals (3-10 years): Moderate risk is okay

- Long-term goals (10+ years): You can be more aggressive

The Bottom Line

This calculator won't make you rich, but it will help you understand how money actually grows.

The most important things about investing aren't finding the perfect product, but:

1. Starting now

2. Staying consistent

3. Making rational adjustments

Einstein supposedly called compound interest "the eighth wonder of the world," but this wonder needs time to work its magic.

I hope this little tool helps you invest with more clarity and confidence.

---

Tool Link: https://compoundinterestcalculator.money/

How to Use It:

- Start with conservative numbers

- Try different scenarios

- Save your calculations

- Come back and recalculate regularly

Investing involves risk. This tool is for calculations only - make your own investment decisions.