Carbon Trading and CCUS Market Growth

Carbon Capture, Utilization, and Storage (CCUS) Market

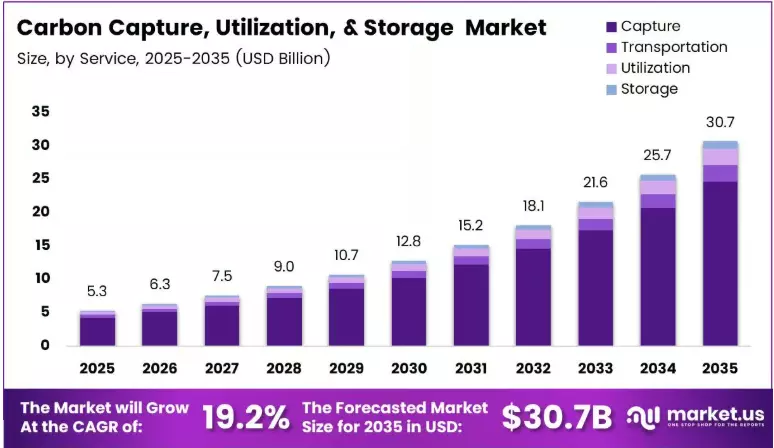

1. Introduction to the Carbon Capture, Utilization, and Storage (CCUS) Market

Carbon Capture, Utilization, and Storage (CCUS) has emerged as one of the most significant technological approaches for reducing greenhouse gas emissions while supporting industrial productivity.

As governments and corporations intensify their commitments to achieving carbon neutrality, CCUS technologies are becoming an essential component of global decarbonization strategies.

The process involves capturing carbon dioxide emissions from industrial facilities and power plants, transporting the captured gas, and either utilizing it in commercial applications or storing it securely in geological formations to prevent atmospheric release.

The growing urgency surrounding climate change has accelerated investments in carbon management technologies across multiple industries.

Heavy-emitting sectors such as cement, steel, chemicals, oil and gas, and power generation increasingly recognize CCUS as a practical pathway to reduce emissions without disrupting existing production infrastructure.

Unlike many renewable technologies that replace fossil fuel-based systems, CCUS complements existing industrial assets by improving their environmental performance.

Market expansion is supported by rising environmental awareness, stricter emission regulations, and significant public and private investments.

Large-scale demonstration projects continue to validate technological feasibility while creating valuable operational experience that supports future commercial deployment. As innovation reduces operational costs and improves capture efficiency, CCUS is transitioning from experimental implementation toward broader industrial adoption.

2. Key Market Drivers, Emerging Trends, and Growth Opportunities

Several factors are contributing to the accelerating growth of the CCUS market. Governments across developed and emerging economies have introduced ambitious climate policies, carbon pricing mechanisms, tax incentives, and financial subsidies to encourage carbon capture deployment.

These initiatives are helping industries offset high capital expenditures while stimulating investment in advanced carbon management infrastructure.

Technological innovation represents another major growth catalyst. Continuous improvements in solvent-based capture systems, membrane separation technologies, cryogenic processes, and direct air capture are significantly enhancing operational efficiency.

Digital technologies, including artificial intelligence, machine learning, and advanced monitoring systems, are optimizing carbon capture performance while improving storage safety and long-term monitoring capabilities.

Beyond emission reduction, carbon utilization is creating entirely new commercial opportunities.

Captured carbon dioxide is increasingly being transformed into synthetic fuels, chemicals, construction materials, polymers, and carbon-based products that generate additional economic value.

This transition toward a circular carbon economy allows industries to convert environmental liabilities into productive resources while strengthening sustainability initiatives.

Growing hydrogen production also presents substantial opportunities for CCUS. Blue hydrogen facilities utilize carbon capture systems to significantly reduce emissions during hydrogen production, supporting the expansion of low-carbon energy ecosystems.

As demand for hydrogen continues to rise in transportation, manufacturing, and electricity generation, CCUS will play an increasingly important enabling role.

Read: Best Stock Market Institute & Trading Courses in India

3. Market Challenges, Competitive Landscape, and Regional Analysis

Despite considerable momentum, the CCUS market continues to encounter several challenges that influence adoption rates. High capital investment requirements remain one of the most significant barriers, particularly for industries operating under narrow profit margins.

Building capture facilities, transportation pipelines, compression stations, and long-term storage infrastructure requires extensive financial resources and long project development timelines.

Technical complexity also presents operational challenges. Every industrial process produces carbon dioxide under different conditions, requiring customized capture technologies tailored to specific applications.

Ensuring the integrity of underground storage sites demands sophisticated geological assessments, continuous monitoring, and rigorous regulatory compliance to maintain long-term environmental safety.

The competitive landscape continues to evolve as technology providers, engineering companies, energy corporations, and research organizations establish strategic partnerships to accelerate innovation.

Companies increasingly focus on improving capture efficiency, reducing operating expenses, and developing integrated carbon management solutions that combine capture, transportation, utilization, and storage within unified project ecosystems.

Regionally, North America currently maintains a leading position due to established regulatory support, extensive pipeline infrastructure, and substantial government funding programs.

Europe follows closely with aggressive climate policies and strong investments in industrial decarbonization initiatives.

Meanwhile, Asia-Pacific is emerging as one of the fastest-growing markets, driven by rapid industrialization, expanding manufacturing sectors, and increasing governmental emphasis on carbon reduction. Latin America, the Middle East, and Africa are also beginning to invest in CCUS projects as part of broader energy transition strategies.

4. Future Outlook of the Carbon Capture, Utilization, and Storage (CCUS) Market

The future of the CCUS market appears highly promising as nations intensify efforts to achieve long-term climate objectives.

Continued investment in research and development is expected to improve capture efficiency, lower operational costs, and expand the range of commercially viable carbon utilization applications.

As economies pursue net-zero emissions, CCUS will increasingly complement renewable energy sources by addressing emissions from sectors where complete electrification remains technically challenging.

Investment activity is expected to remain robust, supported by government funding, private equity participation, institutional investors, and multinational energy companies.

Financial markets increasingly recognize CCUS as a strategic climate technology capable of delivering measurable emissions reductions while supporting industrial competitiveness. Growing collaboration between public institutions and private enterprises will further accelerate commercialization and infrastructure development.

Integration with emerging technologies will define the next phase of market evolution. Artificial intelligence, digital twins, predictive analytics, automation, and advanced monitoring systems will improve operational reliability while reducing maintenance costs.

Simultaneously, the expansion of carbon transportation networks and geological storage facilities will strengthen the scalability of large-scale deployment.

Looking ahead, the Carbon Capture, Utilization, and Storage (CCUS) market is expected to become a cornerstone of global decarbonization efforts. Its ability to reduce industrial emissions, enable cleaner energy production, foster innovation, and create new economic opportunities positions it as a critical technology for achieving sustainable development.

As policy support, technological advancements, and investment continue to converge, the CCUS market is poised for sustained growth and increasing importance in the transition toward a low-carbon global economy.